Private Credit: Wider Spreads, Higher Rewards

Why investors should consider opportunities in private credit, where spreads remain significantly wider than public credit.

High-yield bonds have long been considered a core component of fixed-income portfolios. In absolute terms, the high-yield bond market might still appear compelling. At 6.88%, yields are currently about 50 basis points higher than their median level over the past decade.

Thinking about yields this way, however, offers an incomplete picture of the asset class. When making allocation decisions, what matters is not a bond’s yield in absolute terms, but its yield relative to other potential opportunities.

One way to analyze yields on a relative basis is to look at a bond’s yield compared to the rate offered on US Treasury securities. The market yield on a 10-year US Treasury, for instance, is currently 4.3%. Since Treasuries are highly liquid assets with almost zero chance of default, investors can earn this rate risk-free.

For bearing the risk of investing in non-Treasury bonds, investors can expect to earn a yield above this risk-free rate. In fixed-income parlance, this additional compensation is known as a “spread.” And, while yields might be high in the current environment, spreads are remarkably low.

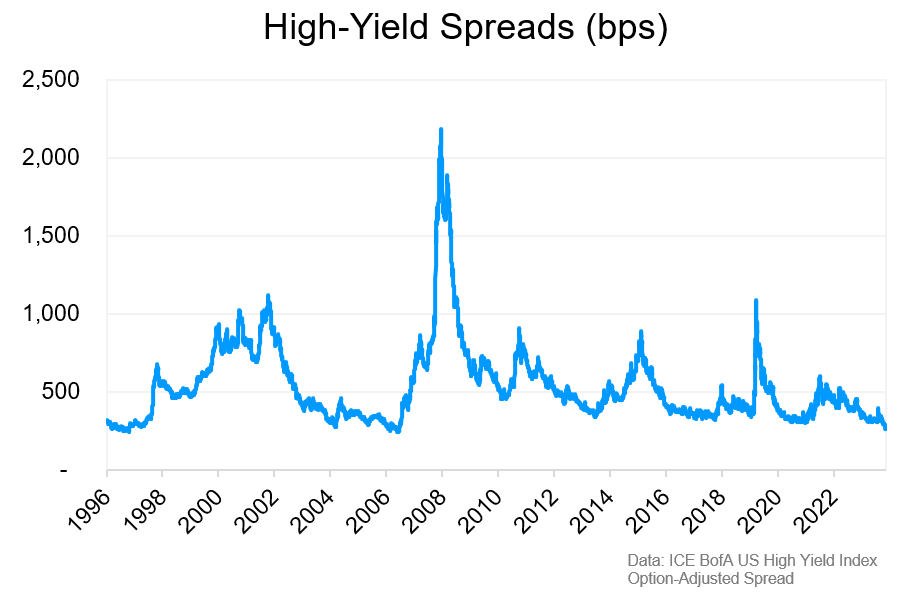

Spreads Are Historically Low

In November, the average spread between maturity-matched Treasuries and high-yield bonds fell to 263 basis points. This is a historically low level. In fact, spreads have been beneath their current level for just 1.6% of all trading days since 1997.

According to Bloomberg research, high-yield bonds have averaged an annual default rate of 1.8% since 2000. In recessions, this figure can eclipse 5%. But due to slim spreads, investors in public high-yield markets are earning little additional compensation for bearing these risks. This makes high-yield bonds much less competitive as a fixed-income component.

Why have high-yield spreads compressed so significantly in recent years? One possible explanation could be the emergence of high-yield ETFs. These funds make the asset class more accessible to retail investors, who are drawn in by high nominal yields. This increased demand pushes up asset prices and leads to lower-than-average yields for bearing the same risk.

The ETF story could also help explain why investment-grade spreads have fallen substantially in recent years. But while this dynamic has compressed spreads in many fixed-income asset classes, there is one area in which spreads are noticeably wider – private credit.

Private Credit Spreads Remain Wide

Private credit spreads are much wider than public credit spreads. The Apollo Diversified Credit Fund, for instance, which invests in a portfolio of private credit verticals, has a portfolio yield of 8.6%. That reflects a 440 basis point spread above the 5-year Treasury (most private credit loans have a maturity of 5 years or less).

Like many private market asset classes, it can be challenging to aggregate data in private credit. Research from both Deutsche Bank and Goldman Sachs, however, confirms that private credit spreads generally range between 300 and 600 basis points.

Of course, earning a spread is rarely a free lunch. Spreads generally exist to compensate investors for bearing some form of risk. Considering that many private credit loans are made to smaller or unrated companies, these loans do come with default risk.

Historically, however, private credit has had lower loss ratios than high-yield bonds. This means that private credit spreads more than compensate for default risk based on historical averages. In fact, higher private credit spreads are primarily compensating for the illiquidity of the asset class.

Private credit assets are more challenging to sell, meaning that investors may need to be patient when exiting a position. Since many investors hold the majority of their fixed-income positions for years, however, private credit can offer an attractive opportunity to harvest this “illiquidity premium.” Moreover, we believe that private credit spreads incorporate some level of genuine alpha resulting from regulatory restrictions on bank lending activity.

Private Credit’s Outperformance

As a direct result of these outsized spreads, private credit has historically outperformed public credit asset classes. The aforementioned Apollo fund, for instance, has returned 5.9% annualized over the past five years. In comparison, the high-yield ETF HYG has returned 3.5% over that same time frame. Other private credit funds have performed even better, with the Ares Capital Corp BDC posting 10.2% returns.

The attractiveness of these performance figures has resulted in rising interest from retail investors. Recently, institutional managers like KKR and Apollo have introduced public fund structures to meet this demand. If the supply of funds from retail overwhelms demand from creditworthy borrowers, lending standards among fund managers could fall. As private credit grows in popularity, we have already seen inexperienced managers come in with inadequate credit underwriting capabilities. This makes it essential for investors to be selective about their manager of choice.

Accessing Private Credit Investments

Despite its name, private credit is gradually becoming a more accessible asset class to public investors. Closed-end funds like BDCs and interval funds are increasingly popular structures to invest in private credit assets. Generally, open-end funds like ETFs are poorly suited to private credit due to the illiquidity of the underlying assets.

At Sandro Wealth Management, we specialize in analyzing private credit investments and helping Accredited Investors & Qualified Purchasers navigate the market. For those who have the capacity and willingness to invest in private credit, we believe that this asset class can offer compelling opportunities compared to traditional high-yield investments.

Related INSIGHTS