Accessing Private Asset-Backed Finance

Apollo’s Asset Backed Credit Company (ABC) can potentially offer higher current income while maintaining investment grade exposure.

In the wake of the Global Financial Crisis, policymakers around the world tightened bank regulations considerably. While this may have made banks safer, it also dramatically constrained bank lending. After 2008, the annual growth rate of US bank loan portfolios shrank to less than half pre-crisis levels.

To fill this lending gap, private credit expanded to provide new sources of debt financing to borrowers. Direct lending to companies, once the exclusive domain of banks, has been private credit’s largest growth area. Increasingly, however, private credit is expanding beyond direct lending.

Today, private credit is capturing lending share in the asset-backed finance (ABF) market. This sector of fixed income involves lending against particular pools of assets. Because ABF is based on the collateral value and cash flow of the underlying assets, it can come with unique benefits for investors.

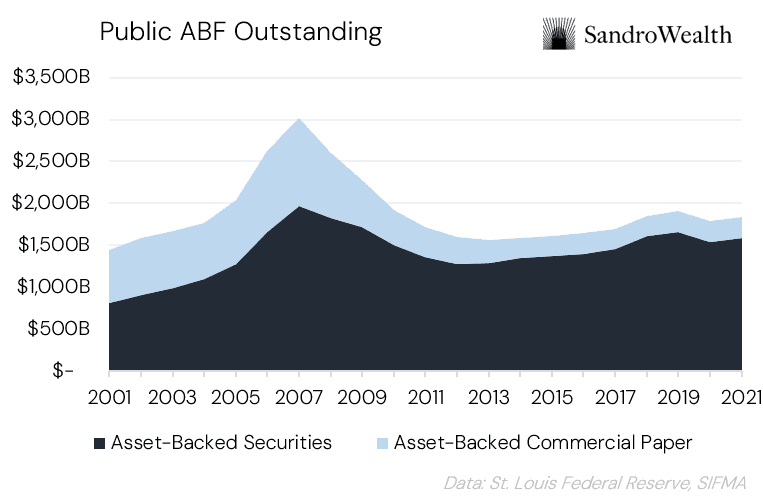

We can measure the size of the traditional ABF market by looking at public asset-backed securities and bank-sponsored asset-backed commercial paper. Based on the volume of assets outstanding, this market has shrunk significantly since the financial crisis.

Much like in direct lending, constraints on banks have created the opportunity for private credit to step in. Non-bank financing currently constitutes just a third of the US ABF market, indicating significant room for growth. Moreover, secular drivers such as increased demand for infrastructure financing and flexible lending solutions point to an ample pipeline of assets.

In this article, we explore the opportunity for investing in private credit asset-backed finance. We begin by understanding the asset class as a whole, followed by analyzing the market’s key benefits when compared to traditional fixed income. Finally, we look at the Apollo Asset Backed Credit Company, a compelling way for investors to access the rapidly growing private ABF market.

What is Asset-Backed Finance?

In fixed-income markets, investors are likely most familiar with ‘issuer-backed debt’. This type of debt is raised by companies or governments to fund their operations and is backed by the full faith & credit of the issuer. Examples of issuer-backed debt include Treasuries, municipal bonds, and bonds issued by blue-chip firms like Apple.

Although issuer-backed debt is popular, it is not the only type of fixed-income investment on the market. In contrast to debt that funds specific issuers, some debt raises money to fund specific assets. This is the $15 trillion ‘asset-backed debt’ market, more commonly known as asset-backed finance.

What kind of assets do ABF instruments fund? Historically, residential mortgages have been the most popular assets, giving rise to the $11 trillion mortgage-backed securities market. Today, however, the ABF universe also includes assets like car loans, student loans, equipment leases, infrastructure financing, and even music royalties.

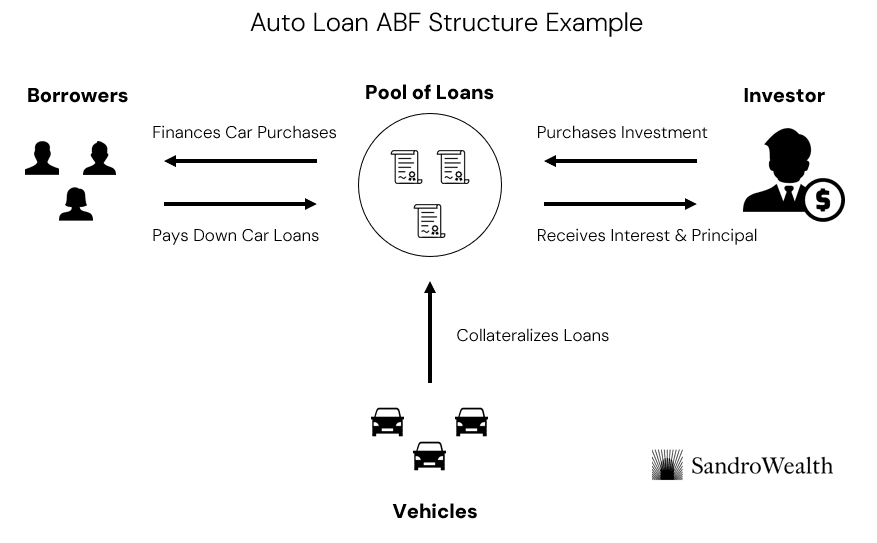

In a typical issuer-backed structure, the cash flows to pay interest and principal come from the issuer’s ongoing operations (such as profits or tax receipts). ABF structures, however, derive their cash flows from the underlying pool of assets. In an auto loan or mortgage ABF note, for instance, interest and principal payments on the underlying loans pass through to investors as coupon payments. As a form of secured lending, investors also have recourse to the collateral value of the assets, such as the underlying vehicles or homes.

Another key difference is that ABF assets are typically self-amortizing. Much like a residential mortgage, interest and principal are paid down together over time. In contrast, issuer-backed debt often comes with a large principal payment at maturity, which can introduce rollover risk if an issuer needs to refinance their debt.

Benefits of Private ABF Investing

As a form of private credit, private ABF captures many of the benefits of the broader asset class. These include higher spreads relative to public benchmarks and lower historical loss rates. These advantages are fundamentally driven by illiquidity premiums, lending flexibility, and the capacity for manager-driven alpha in a relatively fractured market. Within the private credit universe, however, ABF can also come with some unique benefits.

First, asset-backed strategies are imperfectly correlated to public bonds. Simply put, the factors that may affect the value of assets like auto or mortgage loans are generally distinct from those that influence the health of corporate borrowers. Across the investment-grade ABF universe, correlation to US corporates has generally averaged around 0.5-0.6 over the past decade. This means ABF may offer compelling diversification benefits within a fixed-income allocation.

Next, ABF investments come with unique structuring benefits that can help minimize loss rates. Thanks to protective covenants, diversified underlying asset pools, and the security offered by a bankruptcy-remote legal structure, ABF assets are generally highly robust to financial shocks. In fact, between 2011 and 2021, the investment-grade ABS market did not experience a single default.

Finally, ABF assets may help improve the inflation resiliency of an investor’s portfolio. For ABF backed by hard assets, such as infrastructure or equipment, collateral value tends to rise with inflation, offering greater security. Moreover, the majority of ABF securities are floating-rate instruments, meaning yields can rise if central banks raise rates in response to price pressures.

To illustrate the potential advantages of a floating-rate allocation, consider the historical performance of two ETFs with comparable maturity and credit profiles: FLOT, which tracks an index of floating-rate bonds, and IGSB, which tracks an index of fixed-rate bonds. In 2022, the yield on a two-year Treasury climbed approximately 360 basis points. That year, IGSB fell -5.71%, but FLOT delivered a positive return of 1.23%.

Like all private market investing, however, accessing the benefits of private ABF is contingent on finding quality and experienced managers. For investors interested in pursuing this asset class, Apollo’s Asset Backed Credit Company is a highly compelling option.

ABC: Apollo’s Asset-Backed Finance Fund

As one of the world’s largest alternative asset managers, Apollo needs little introduction. The firm has over $750 billion in assets under management and operates strategies across credit, equity, and real asset verticals. Within the ABF space, Apollo offers the Asset Backed Credit Company (ABC), an unlisted fund open to high-net-worth investors.

ABC’s investment approach is similar to the strategy employed by Apollo’s other private credit funds. The fund leverages Apollo’s origination capabilities to source off-market credit deals and manages those assets over time to optimize returns. Apollo has more than 4,000 employees focused on originating asset-backed opportunities, generating more than $75 billion in annual volume.

As the firm has articulated, this focus on origination helps Apollo generate greater returns for a given level of credit risk. Across the firm’s entire asset-backed portfolio, Apollo aims for 100-250 basis points of excess annual return over corporate credit. At the same time, the firm’s asset-backed portfolio has maintained a low historical loss rate of just 1.3 basis points, compared to about 10 basis points for BBB corporate bonds.

In part, this excess return also stems from a structuring premium associated with Apollo’s asset management skills. Effectively analyzing and valuing asset-backed investments requires sophisticated knowledge and expertise not widely found in the financial industry. Moreover, ABC benefits from several unique tax advantages that may help increase an investor’s net return. While ABC does not currently employ leverage, the fund is expected to utilize leverage of approximately 0.1-0.3x portfolio assets over a cycle, potentially further boosting returns.

Although ABC can invest across the asset-backed universe, the fund centers on five key pillars: consumer finance, residential mortgage loans, commercial real estate, hard assets, and financial assets. Similarly, the fund focuses largely on the investment-grade (IG) universe, although it may opportunistically invest in lower-rated instruments. As of March 2025, ABC’s portfolio was ~80% IG or IG-equivalent, with 77% of the fund’s assets stemming from direct or partner originations.

How Can ABC Benefit a Portfolio?

Due to ABC’s excess return target over public bonds and capacity for diversification, the fund can likely be a valuable portfolio addition for many investors. In Sandro Wealth’s view, however, investors with income generation targets are most likely to benefit from ABC. Due to the fund’s high current yield and investment-grade exposure, ABC can allow investors to allocate more of their portfolio to growth opportunities, potentially resulting in greater future wealth.

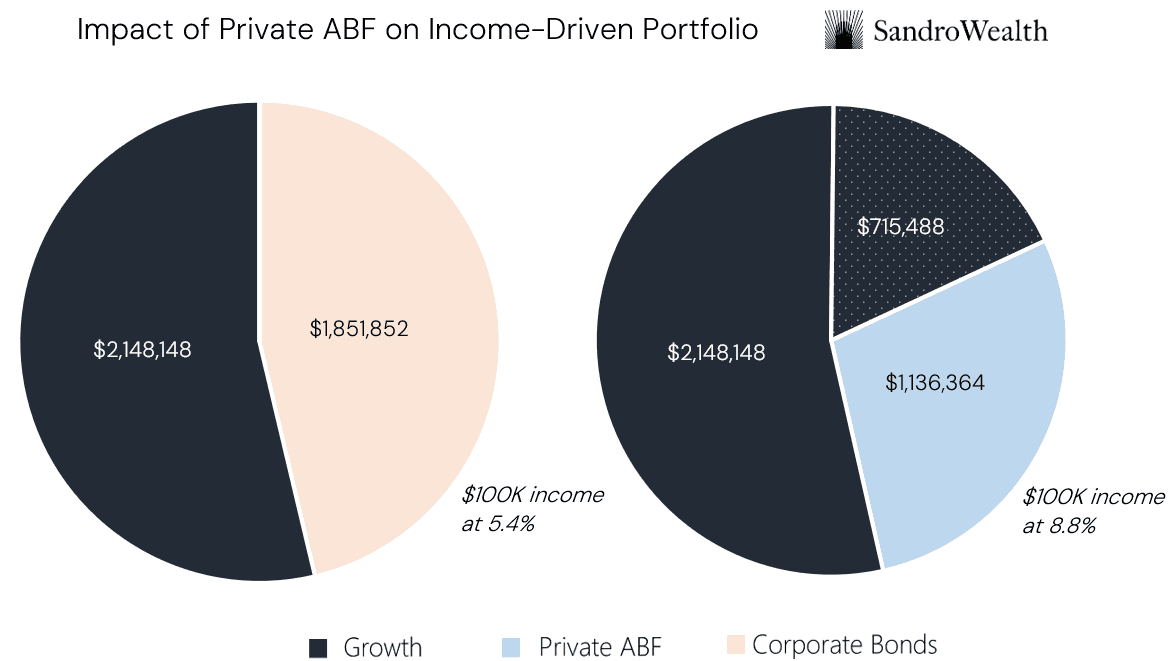

As of March 2025, ABC’s portfolio yield averaged 8.8%, compared to a BBB corporate bond yield of approximately 5.4%. This spread reflects ABC’s excess return target and means that investors can potentially earn equivalent income with a lower capital commitment.

For example, consider an investor with a $4 million total portfolio and an income generation target of $100,000 annually. To achieve this target with just investment-grade corporates, this investor would need to hold about $1.85 million in public bonds at a 5.4% yield. This amounts to 46.3% of their total portfolio.

In comparison, an equivalent investor who aims to achieve their income targets with ABC would need to commit about $1.14 million at an 8.8% yield, just 28.4% of their portfolio. Essentially, the ABC investor has freed up more than $700,000 to commit to high-return growth investments, while maintaining approximately 80% exposure to investment-grade assets.

In terms of long-run outcomes, this additional growth sleeve can contribute to significant excess wealth generation. Suppose that an investor can earn 15% annually on growth assets and 10% annually on income assets. Compounded over a five-year period, maintaining $715,000 in growth over income results in $286,000 in additional final wealth.

ABC’s corporate structure also allows the majority of fund income to be taxed as qualified dividends, rather than traditional interest taxed at ordinary income rates. This structuring can potentially reduce an investor’s effective tax rate paid on fund returns by about 5 to 10 points, although individual situations may vary. Investors have the option to receive a 1099 or a K-1 for tax filing purposes.

Of course, it is unlikely for an investor to commit their entire fixed-income or income-generating allocation to one asset class, much less one fund. This illustrative example demonstrates, however, the advantages of private market exposure paired with a modernized strategic asset allocation approach.

Conclusion

Due to ABC’s potential for excess income generation and diversifying portfolio benefits, we believe it may be a good fit for investors seeking additional private credit exposure. Understanding how this fund fits into the context of an entire portfolio, however, requires guidance from a partner with deep experience in and knowledge of private markets. At Sandro Wealth Management, we specialize in working with advisors and their clients to navigate private markets, helping investors utilize asset classes like private ABF to achieve their portfolio goals.

ABC is currently open to Accredited Investors with a minimum investment size of $2,500 for all share classes. Most share classes pay a 1% management fee and an incentive fee of 10% with a 5% hurdle. The returns described in the preceding discussion are net of fees, and so these fees do not change our analysis.

Like all private market investing, ABC comes with unique risks. Notably, capital redemptions are limited to up to 5% of the fund’s outstanding value on a quarterly schedule, meaning ABC is less liquid than traditional investments. And while Apollo has been active in the asset-backed market for decades, ABC was only launched in 2024, making it a relatively new fund.

For investors comfortable with these risks, however, both ABC and the private ABF market can offer compelling potential advantages for an investor’s portfolio. If you’re interested in learning more about this investment opportunity or private market investing as a whole, we invite you to reach out to Sandro Wealth Management.

Related INSIGHTS