Infrastructure is essential to the functioning of the modern economy. But amid strained government budgets, these assets are facing a historic investment shortfall. Private capital has become increasingly essential to finance the roads, power grids, data centers, and renewable energy projects that modern economies require.

For investors, this structural imbalance presents a compelling opportunity. Private infrastructure assets have historically demonstrated both strong performance and robust resilience. The magnitude of capital now required is broadening access to an asset class long reserved for pensions and sovereign wealth funds.

Accessing private infrastructure has traditionally required institutional scale and a tolerance for complex structures. The KKR Infrastructure Conglomerate LLC (K-INFRA) offers a different approach: an evergreen vehicle that provides exposure to KKR’s global infrastructure platform through a structure designed for individual investors. In this article, we examine the case for private infrastructure, its role within a diversified portfolio, and how KKR’s 49 years of experience can help deliver value for investors.

The Case for Private Infrastructure

Infrastructure encompasses the essential systems that economies require to function, such as transportation, utilities, energy, networking, and industrial facilities. These assets represent the base layer upon which daily life and business depend. Private infrastructure investing involves taking unlisted equity or debt positions in the companies that own and operate these systems.

Several characteristics distinguish infrastructure from other private market asset classes:

Demand Inelasticity. Infrastructure assets provide essential services that are required through market cycles. Households and businesses continue to need power, connectivity, and transportation regardless of broader economic conditions. This essential nature creates relatively consistent demand profiles even during periods of stress.

Revenue Predictability. Infrastructure revenues are frequently underpinned by long-term contracts, government regulation, or structural market positions. A telecom operator may hold a 30-year master agreement with an investment-grade tenant; a utility may earn regulated returns approved by a public commission. These arrangements provide long-term cash flow predictability that is uncommon in traditional investments.

Inflation Protection. Many infrastructure contracts include explicit inflation escalators or allow operators to pass through rising costs to customers. Regulated utilities often receive approved rate increases tied to inflation, while contracted assets may feature annual price adjustments indexed to CPI. This pricing power can help preserve real returns during inflationary periods.

Private infrastructure is not without risks, especially related to valuation uncertainty and illiquidity. Historically, however, these characteristics have translated into distinct benefits when private infrastructure is held within a broader portfolio.

Private Infrastructure’s Role in a Portfolio

Private infrastructure is not a direct substitute for stocks or bonds – it can complement either asset class. Conservative investors may fund their allocation from equities, using infrastructure’s stability to dampen portfolio volatility. Growth-oriented investors may fund their allocation from fixed income, seeking higher return potential while retaining income characteristics.

Because private infrastructure can help a portfolio achieve distinct goals, the right choice depends on an investor’s risk tolerance and objectives. In either case, it’s important for infrastructure investors to align their holding period with the long-term nature of the underlying assets. Below, we consider private infrastructure in the context of a broader portfolio, looking at how this asset class can potentially help meet investor goals.

Capital Preservation

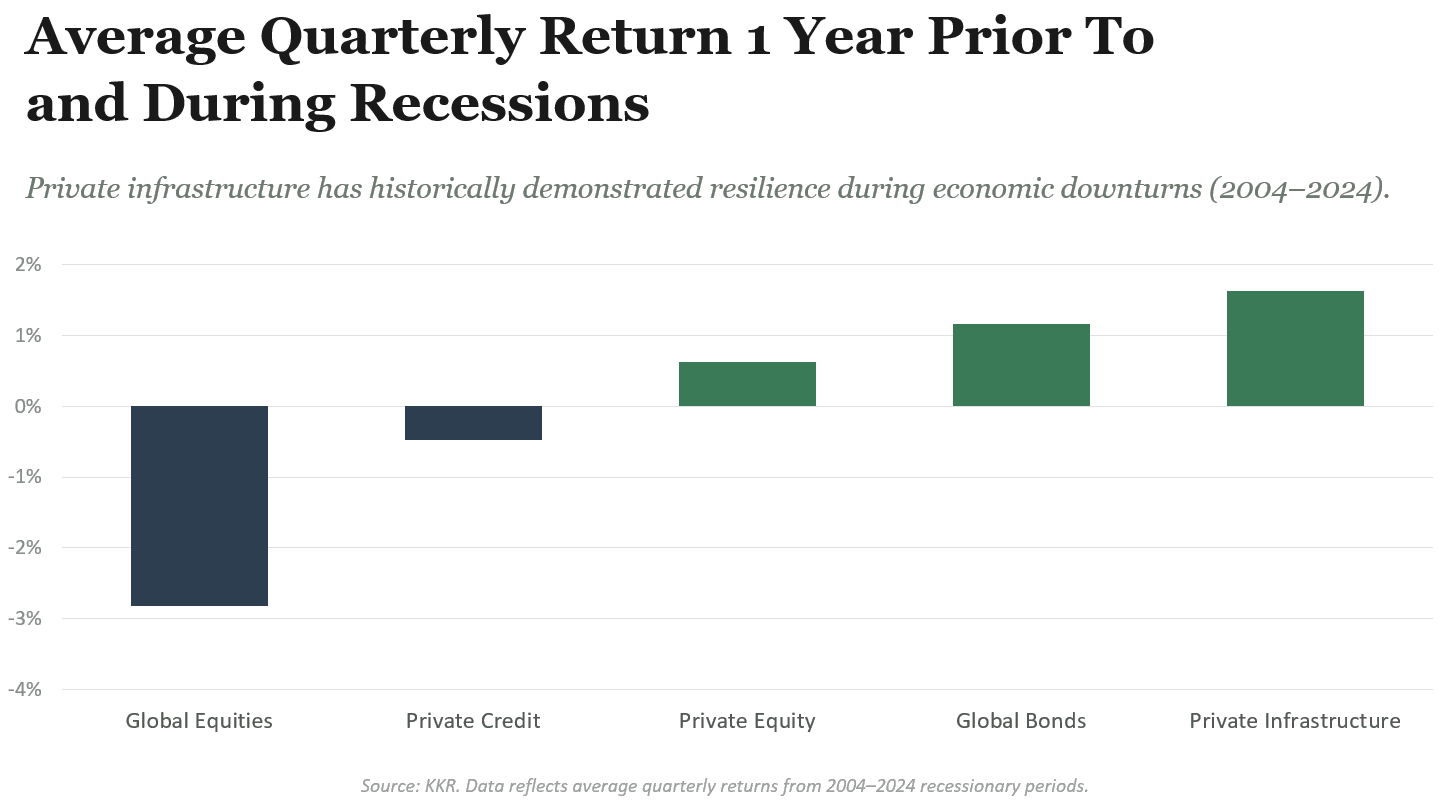

The essential nature of infrastructure services, combined with the hard asset base underlying most investments, provides a tangible foundation for value. During the 2008 financial crisis and subsequent market dislocations, private infrastructure demonstrated greater resilience than public equities, listed infrastructure, and private real estate. This defensive quality largely stems from demand inelasticity: when economic conditions deteriorate, consumers may reduce discretionary spending, but they need to continue paying their utility bill.

Income Generation

Infrastructure assets frequently produce steady cash distributions supported by contracted or regulated revenues. Unlike fixed-income instruments, however, these distributions often grow over time as contracts escalate with inflation or as operators expand. For clients seeking current income with potential for growth, infrastructure can serve as a complement to traditional bond allocations.

Diversification

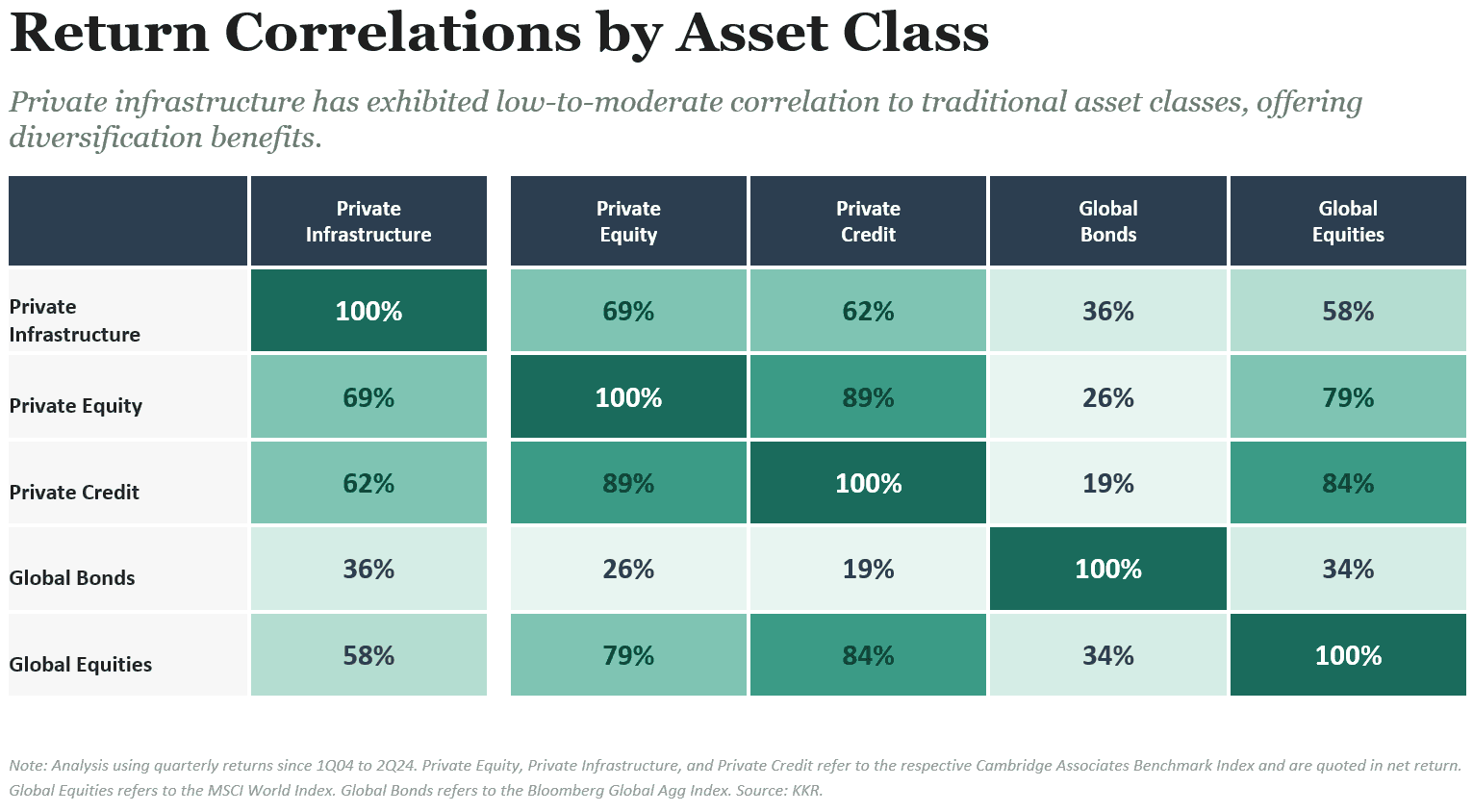

Private infrastructure has historically exhibited low-to-moderate correlation to both public equities and fixed income. Adding an asset class with differentiated return drivers can potentially improve a portfolio’s risk-adjusted performance, smoothing returns across market environments without sacrificing long-term growth.

KKR’s Infrastructure Platform

Infrastructure investing requires specialized expertise. Unlike public equities, where information is widely available and markets are relatively efficient, private infrastructure demands sector knowledge, deal access, and operational capabilities. As a result, manager selection matters considerably in this asset class.

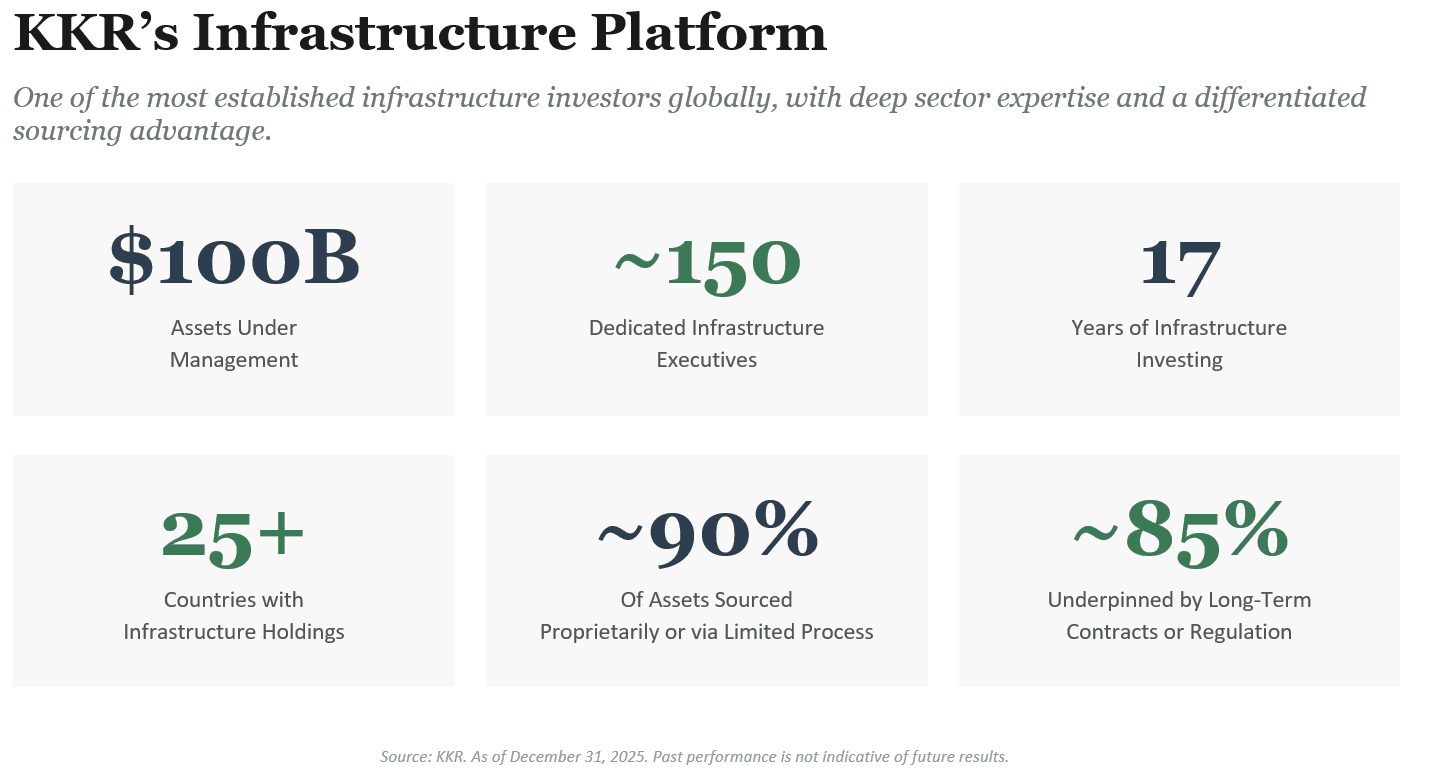

KKR is among the most established names in private markets, with over 49 years of investment experience across private equity, credit, and real assets. The firm established its dedicated infrastructure platform in 2008 and has since grown it to $100 billion in assets under management. Approximately 150 executives work on KKR’s dedicated infrastructure team across North America, Europe, and Asia Pacific.

Source: KKR

This experience has translated into a differentiated investment approach. 90% of KKR’s infrastructure investments have been sourced proprietarily or through limited competitive processes – a function of the firm’s longstanding corporate relationships and global presence. Once invested, approximately 85% of assets within KKR’s infrastructure strategies are underpinned by long-term contracts or government regulation, reflecting a disciplined focus on revenue predictability and downside protection.

Historically, individual investors have been unable to access the managerial expertise needed to effectively invest in infrastructure – typically due to high minimums, long lock-ups, and complex structures. K-INFRA changes that, providing access to KKR’s infrastructure capabilities through a streamlined structure designed for individual investors.

K-INFRA: Accessing KKR Infrastructure

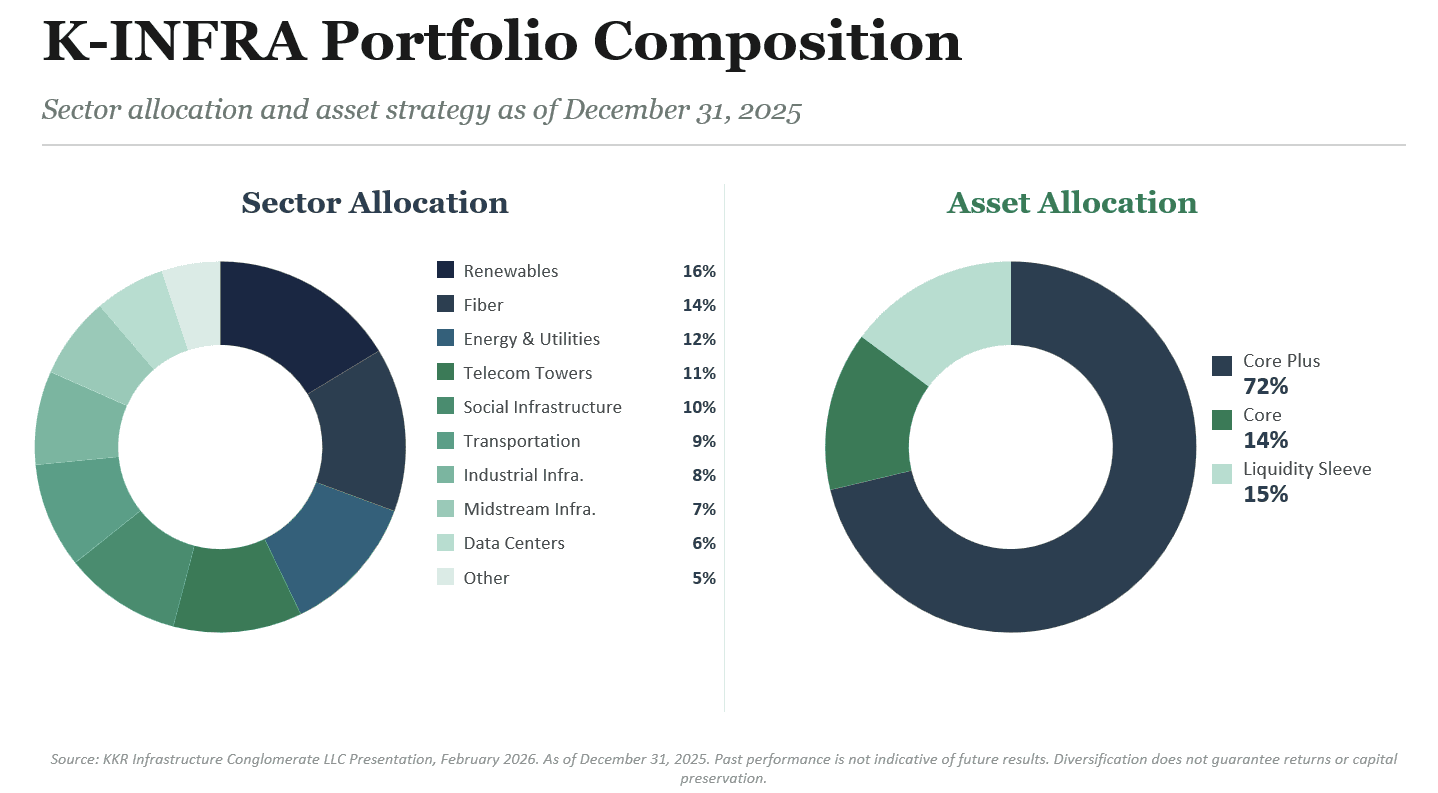

The KKR Infrastructure Conglomerate LLC (K-INFRA) provides Accredited Investors with direct exposure to KKR’s global infrastructure platform through a structure designed specifically for individuals. As of December 31, 2025, the fund held a transactional net asset value of $6.47 billion across 32 infrastructure holdings spanning ten distinct sectors and more than 25 countries. K-INFRA has a target net return of 9-11% per year with a target annualized distribution of 4-5%.

Source: KKR

What distinguishes K-INFRA is the fund’s direct investment approach. Rather than allocating to third-party managers, K-INFRA takes controlling or influential positions in infrastructure assets. This allows KKR to drive operational improvements, optimize capital structures, and create value throughout the holding period, an approach that has defined the firm’s private equity heritage for decades.

K-INFRA’s portfolio reflects a thematic approach organized around three secular trends:

Digitization. The accelerating global demand for connectivity and data processing drives allocations to fiber networks, telecom towers, and data centers. Global expenditure on digital infrastructure is expected to reach nearly $4 trillion next year.

Decarbonization. The ongoing energy transition creates opportunities in renewables, utilities, battery storage, and grid modernization. Global energy demand jumped 2.2% in 2024 alone, underscoring the need for continued investment in both conventional and renewable power infrastructure.

Deconsolidation. Corporations and governments are increasingly divesting non-core infrastructure assets, creating acquisition opportunities for private capital with the expertise to own and operate these systems.

As of December 31, 2025, K-INFRA’s Class R shares had delivered an inception-to-date annualized net return of 11.64% and a Q4 2025 annualized distribution rate of 4.27%. While past performance is not indicative of future results, these figures demonstrate the fund’s capacity to generate both capital appreciation and current income.

The fund’s structure addresses several friction points that have historically limited individual investor access. First, capital is fully drawn upon investment, eliminating the capital call management associated with traditional drawdown funds. Next, the evergreen structure allows realizations to be reinvested automatically, enabling long-term compounding. Finally, K-INFRA intends to offer quarterly liquidity for up to 5% of aggregate NAV, providing a degree of flexibility.

Conclusion: Key Considerations for Private Infrastructure

Private infrastructure offers a compelling combination of capital preservation potential, income generation, and diversification benefits. K-INFRA provides a vehicle through which investors can access these characteristics via KKR’s established platform and a structure designed for individual investors. However, the asset class is not without risk.

Infrastructure investments are illiquid by nature, and while K-INFRA intends to offer quarterly repurchases, there is no guarantee that redemption requests will be fulfilled in full or at all. The fund also employs leverage, which can magnify both gains and losses. Moreover, infrastructure assets are uniquely exposed to political and regulatory developments, such as changes in permitting requirements or utility rate structures.

For those who can accept these limitations, K-INFRA warrants consideration as part of a diversified portfolio. K-INFRA charges a 1.25% annual management fee and a 12.5% performance participation allocation with a 5% hurdle. A 5% early repurchase fee also applies if investors liquidate their position within the first two years.

At Sandro Wealth Management, we specialize in helping advisors and their clients evaluate private market opportunities like K-INFRA. If you’re interested in learning more, we invite you to reach out through our website for an initial consultation. As global infrastructure needs continue to expand, this asset class may offer investors a differentiated source of returns, income, and portfolio resilience.

Disclaimer

Sandro Wealth Management, LLC (“Sandro Wealth”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where Sandro Wealth and its representatives are properly licensed or exempt from licensure.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Targets are estimates based on certain assumptions and analysis made by the Advisor. There is no guarantee that the estimates will be achieved.

Although bonds generally present less short-term risk and volatility risk than stocks, bonds contain interest rate risks; the risk of issuer default; issuer credit risk; liquidity risk; and inflation risk.

Diversification does not ensure a profit or guarantee against loss. Past performance shown is not indicative of future results, which could differ substantially.

Investing in private funds involves a risk of loss that each existing and prospective investor should understand and be willing to bear. Existing and prospective investors are reminded to read fully and carefully understand these risks as outlined in Offering Documents and to discuss these risks with the Advisor.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor's particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

This article was independently prepared by Sandro Wealth Management LLC for educational purposes only. KKR & Co. Inc. has not reviewed, approved, or endorsed the content herein, nor does this article represent the views of KKR or its affiliates. For official KKR product information, investors should refer to KKR's website and published materials.

No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. All investments include a risk of loss that clients should be prepared to bear. The principal risks of Sandro Wealth Management LLC strategies are disclosed in the publicly available Form ADV Part 2A.