Middle-Market Lending with GCRED: Golub’s Specialist Advantage

Private credit’s structural features offer advantages in middle market lending. We examine the segment and how investors can access Golub’s return-enhancing direct lending strategy.

For much of its history, private credit has been treated as a uniform asset class. Beneath the label, however, the market is composed of sub-sectors with different characteristics. Just as equity investors categorize stocks by market cap, private credit has distinct borrower segments.

The Golub Capital Private Credit Fund (GCRED) offers access to one such segment: direct lending to U.S. middle-market companies. Middle-market lending focuses on financing companies with $10 million to $100 million of EBITDA, which are generally too small to access public debt markets. In this article, we examine how a middle-market allocation can complement large-cap lending – and how GCRED provides access to this segment’s value-add return profile.

Understanding Middle Market Lending

An effective private credit allocation spans a broad range of company sizes, including large-cap, middle-market, and lower-middle-market lending. Each segment offers a differentiated return profile. Allocating across these segments allows investors to access the return premia associated with lending to different-sized borrowers.

With that said, the features that distinguish private credit from public fixed income – including wider spreads, structural protections, and differentiated return drivers – are strongly pronounced in the middle market:

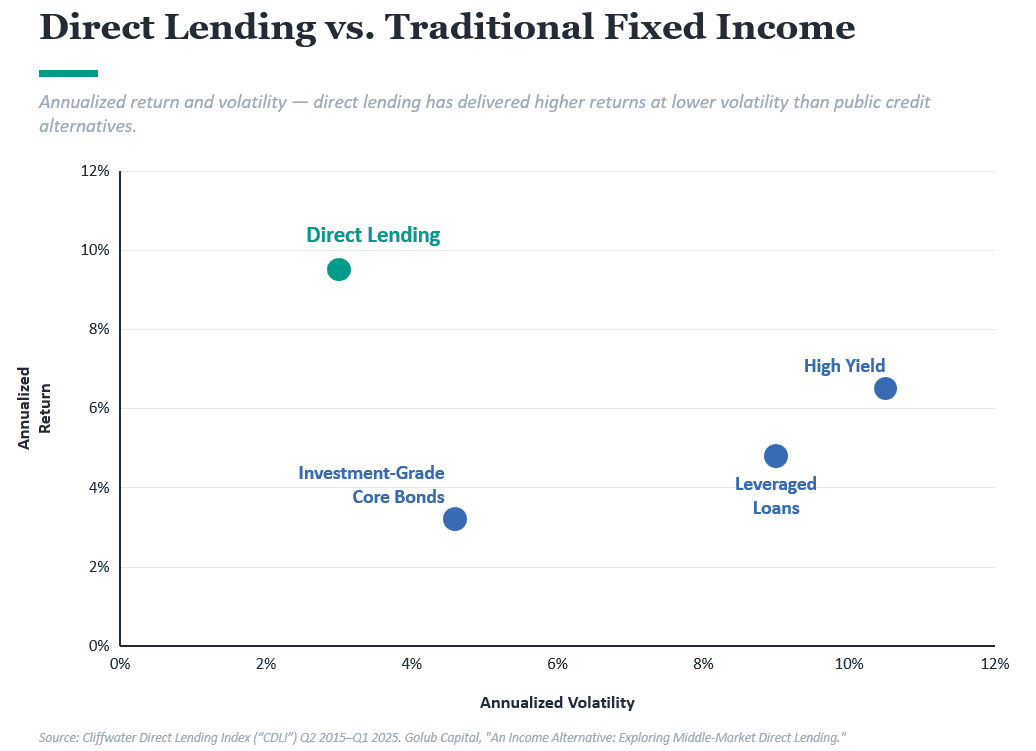

Wider Spreads. In public credit, yield advantages tend to be competed away. But the middle-market universe is vast, made up of over 300,000 individual US businesses. That fragmentation has contributed to wider spreads – over the past decade, middle-market lending has earned an annualized return advantage of roughly 400 basis points over public credit alternatives such as leveraged loans and high-yield bonds.

Structural Protections. In the middle market, deals are directly negotiated between lenders and borrowers. That means lenders can require tighter covenants, customized terms, and more transparent oversight. While smaller companies carry more idiosyncratic risk, structural protections help lenders manage that risk appropriately.

Differentiated Return Drivers. Because smaller firms are generally not represented in public credit allocations, middle-market lending can help diversify an investor’s portfolio by broadening its return drivers. Historically, middle-market loans have exhibited a correlation of 0.3 with US investment-grade bonds.

Because middle-market loans are directly negotiated, the lender’s capabilities shape the outcome at every stage. As a result, a manager’s credit underwriting expertise is closely tied to net returns after defaults and recoveries. The importance of quality is why Golub Capital’s platform – purpose-built for middle-market lending over a 30-year history – stands out.

Golub Capital’s Platform: A Middle-Market Specialist

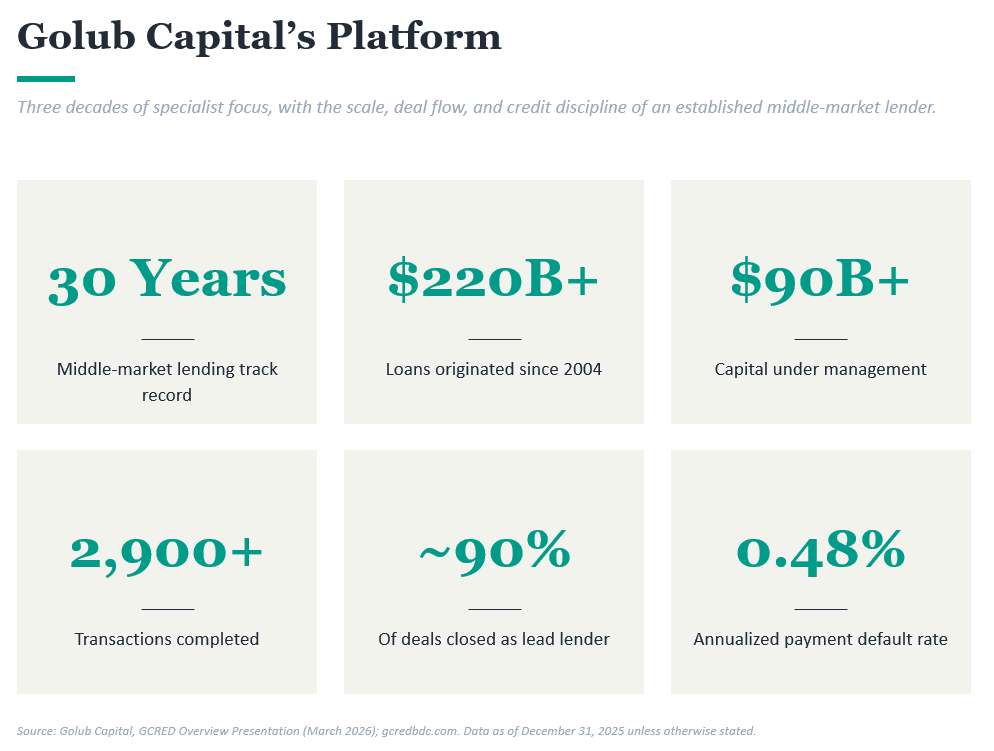

Middle-market lending requires sourcing, underwriting, and monitoring capabilities driven by deep market expertise. Golub Capital has spent three decades developing those capabilities, with a track record that spans over $220 billion in loan originations across more than 2,900 transactions.

Today, Golub is a specialist private credit manager with over $90 billion in capital under management and more than 420 private equity sponsor relationships. The firm serves as lead lender on approximately 90% of the deals it closes – a role that allows Golub to set pricing, shape deal structure, and maintain direct oversight over the life of each loan. Golub has maintained an annualized payment default rate of 0.48% since 2004.

Despite Golub’s scale, the firm’s portfolio remains selective. Golub reviews over 2,000 lending opportunities per year and closes 2-4% of them, reflecting a disciplined diligence process. That selectivity has translated into a compelling track record – Golub has been named Lender of the Year multiple times by Private Debt Investor and received the publication’s Lender of the Decade designation in 2023.

These accolades are not a guarantee of future performance. However, they do showcase Golub’s structural advantages in middle-market lending. For investors, GCRED offers direct access to this specialist platform.

GCRED: Strategy and Portfolio

GCRED invests primarily in directly originated, senior secured loans to U.S. middle-market companies. These loans are generally floating-rate, which limits duration risk. GCRED also focuses on industries that Golub believes are resistant to recessions, providing enhanced resilience.

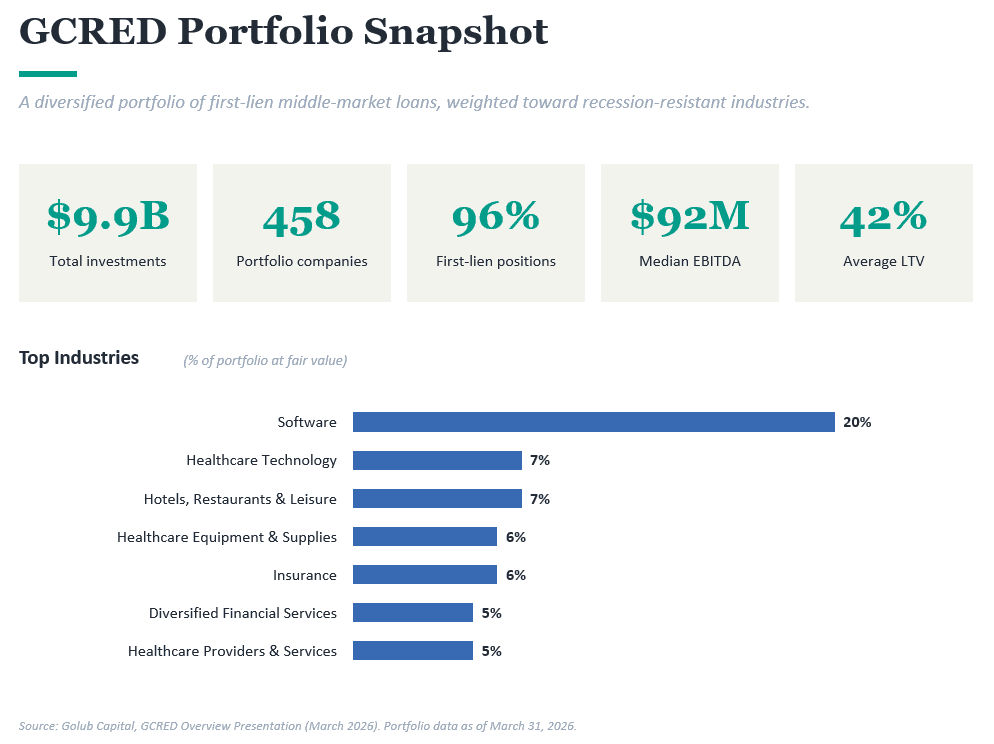

As of March 31, 2026, GCRED held $9.9 billion across 458 portfolio companies, with 96% of the fund invested in first-lien positions. The median borrower generates $92 million of EBITDA, and the average loan-to-value ratio sits at 42%. These characteristics reflect a portfolio built for consistent income generation and capital preservation.

GCRED’s industry exposure further demonstrates Golub’s sector expertise. The fund’s largest concentrations are in software, hospitality, and healthcare technology – segments where Golub has executed hundreds of transactions. These industries share characteristics that suit middle-market lending, including recurring revenue models and durable demand through market cycles.

Finally, GCRED’s position sizing reflects Golub’s continued discipline. The fund’s top ten holdings represent just 13.8% of the portfolio, meaning no single borrower dominates the fund. Diversification across hundreds of companies also limits the impact of any single credit event on the overall portfolio.

GCRED: Performance and Income

GCRED launched in July 2023. Since then, the fund has delivered results consistent with its income and capital preservation objectives.

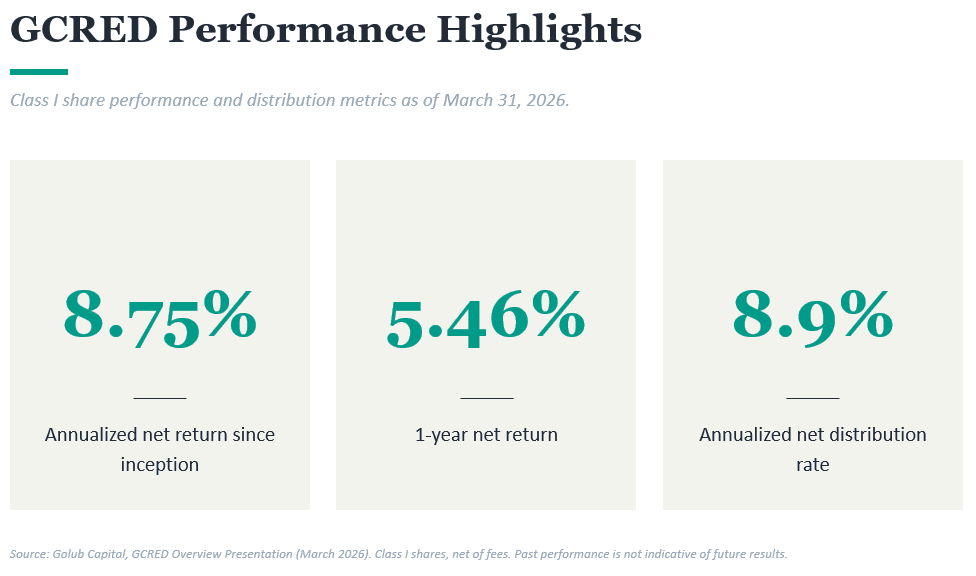

Since the fund’s inception on July 1, 2023, GCRED has generated a net return of 8.75% annualized through March 31, 2026. In the twelve months to March, the fund has delivered a net return of 5.46%. That month, the annualized net distribution rate stood at 8.9%, driven by the fund’s portfolio income.

These results reflect both the structural yield available in middle-market lending and Golub’s execution within the segment. The fund’s floating-rate positioning has allowed income to adjust with prevailing rates, while first-lien seniority and conservative loan-to-value ratios have supported capital stability. Monthly distributions have been funded entirely from cash flows from operations since inception.

Conclusion: An Institutional Platform for Middle-Market Exposure

Middle-market direct lending offers structural features that are increasingly difficult to find in public credit: wider spreads, negotiated protections, and differentiated return drivers. Capturing them requires a manager with the infrastructure to execute at scale. GCRED provides investors with access to that infrastructure through Golub Capital’s 30-year platform.

GCRED is not without certain considerations. The fund is illiquid – shares cannot be freely traded, and quarterly repurchases are capped at 5% of NAV (subject to suspension during periods of market dislocation). GCRED uses leverage, which magnifies both gains and losses. And while default rates in middle-market lending have historically been low, credit losses remain a core risk in any fixed-income strategy.

For investors who can accept these considerations, GCRED’s structural features could be compelling. Monthly subscriptions are accepted with no capital calls. Distributions are paid monthly, with occasional special distributions. The fund comes with a 1.25% management fee and a 12.5% incentive fee.

At Sandro Wealth Management, we help advisors and their clients evaluate private market opportunities like GCRED. If you’re interested in learning more, we invite you to reach out through our website for an initial consultation.

Disclaimer

Sandro Wealth Management, LLC (“Sandro Wealth”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where Sandro Wealth and its representatives are properly licensed or exempt from licensure.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. As a general practice, the first hyperlink or footnote in each paragraph serves as the citation for subsequent figures in that same paragraph, unless covered by a separate hyperlink or footnote.

Targets are estimates based on certain assumptions and analysis made by the Advisor. There is no guarantee that the estimates will be achieved.

Although bonds generally present less short-term risk and volatility risk than stocks, bonds contain interest rate risks; the risk of issuer default; issuer credit risk; liquidity risk; and inflation risk.

Diversification does not ensure a profit or guarantee against loss. Past performance shown is not indicative of future results, which could differ substantially.

Investing in private funds involves a risk of loss that each existing and prospective investor should understand and be willing to bear. Existing and prospective investors are reminded to read fully and carefully understand these risks as outlined in Offering Documents and to discuss these risks with the Advisor.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

This article was independently prepared by Sandro Wealth Management LLC for educational purposes only. Golub Capital LLC has not reviewed, approved, or endorsed the content herein, nor does this article represent the views of Golub or its affiliates. For official Golub product information, investors should refer to Golub’s website and published materials

No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. All investments include a risk of loss that clients should be prepared to bear. The principal risks of Sandro Wealth Management LLC strategies are disclosed in the publicly available Form ADV Part 2A.