For many high-net-worth investors, taxes represent the single largest drag on long-term returns. An investor in the top federal bracket and a high-tax state can lose more than a third of realized gains to taxes. For those holding appreciated stock positions or anticipating a major liquidity event, the challenge is more acute: selling triggers an immediate tax bill, while holding introduces concentration risk.

Long-short tax-aware (LSTA) investing offers a compelling approach to managing these challenges. By combining systematic stock selection with a leveraged structure, these strategies have the potential to deliver competitive returns while also generating substantial tax savings. Below, we look at how LSTA strategies work, where their value comes from, and what investors should weigh before pursuing them.

How It Works: The LSTA Structure

A long-short tax-aware strategy can be thought of as comprising three distinct elements – the initial investment, the short leg, and the long leg. Together, these components form a single, unified portfolio:

1. Initial Investment. The initial investment is what the investor already owns. This could be a diversified portfolio of equities, cash used to purchase securities, or a concentrated stock position that the investor wishes to diversify. These holdings form the core of the portfolio and provide base market exposure, typically benchmarked to a broad index like the S&P 500 or Russell 1000.

2. Short Leg. The short leg is where the structure begins to differentiate itself. The manager borrows shares of stock and sells them in the open market, generating cash. If these stocks decline in value, the investor profits. If they rise, the investor incurs a loss.

3. Long Leg. The long leg nets out the market exposure of the short leg. Proceeds generated from the short sale are used to purchase an equivalent dollar amount of stocks.

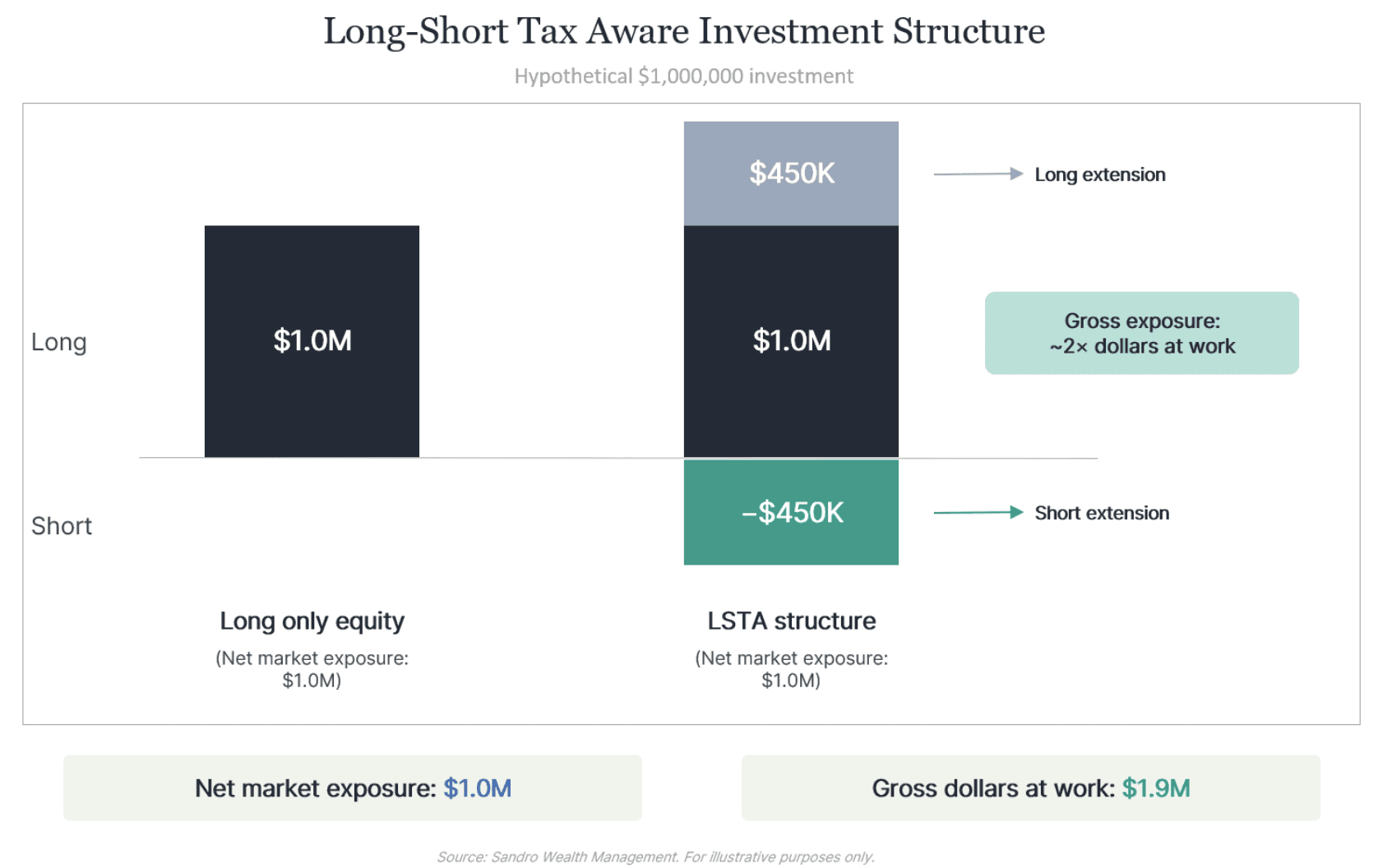

For example, imagine an investor with a $1 million portfolio held in a broad market index. After contributing this amount to an LSTA structure, the manager generates $450,000 in cash through a short sale and uses the proceeds to purchase another $450,000 of stock. Altogether, the investor has $1.9 million in total dollars at work, while net market exposure remains at $1 million.

But if net market exposure remains unchanged, why stretch the portfolio this way? The answer lies in how the stocks within the long and short legs are selected.

The specific positions that make up each leg are determined by a systematic investment model, which evaluates stocks across factors like quality, value, and momentum. Stocks that score well become candidates for the long leg, while stocks that score poorly become candidates for the short leg – an approach with a long track record of academic study and empirical support. This factor selection process is what gives rise to both of LSTA’s core benefits: investment alpha and tax management.

Where LSTA’s Benefits Come From

As the investment model evaluates and rotates positions over time, two benefits emerge. The first is investment alpha: returns above the benchmark generated by the model’s active stock selection. Research suggests that systematic approaches can generate returns that compete favorably with both benchmarks and discretionary active management. The second is tax management: the realization of capital losses that the investor can use to offset gains elsewhere in their financial life. These two benefits arise from the same underlying portfolio mechanics.

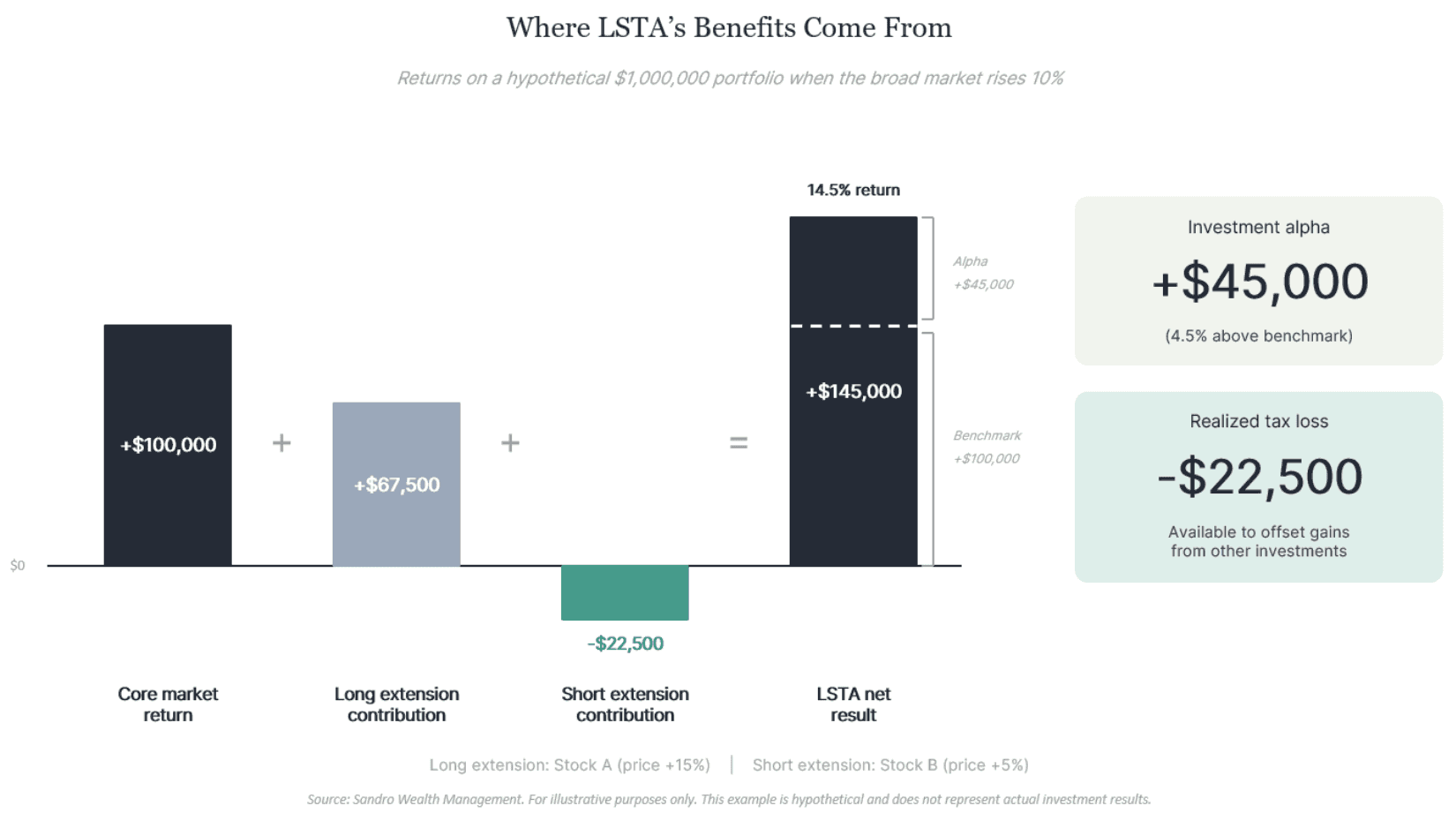

Consider a scenario in which the broad market rises 10% in a given period. During this timeframe, Stock A – which the model selected as a long position – rises 15%. Stock B – which the model selected as a short position – rises 5%.

The model was right about both positions: Stock A outperformed the market, and Stock B underperformed it (short positions generate alpha when they lag the market). That selective positioning is the source of the strategy’s pre-tax investment alpha, with the portfolio returning 14.5% instead of 10%.

But notice what else happened. Even though the model was correct about Stock B’s underperformance, the short position still lost money in absolute terms, since the stock price rose. If that loss is realized, it becomes immediately available to the investor to offset gains elsewhere (such as from a business sale or another liquidity event). In contrast, a tax-smart investor will not realize the gain on Stock A’s long position.

This is the key benefit of an LSTA portfolio. On net, the overall strategy makes money when the market rises, generating both capital gains and capital losses in the process. However, only the losses are realized, not the gains – resulting in tax savings.

In practice, the model holds hundreds of positions on each side. This creates a continuous stream of rotation opportunities – and with each rotation, the model can choose the most tax- efficient path. Importantly, the strategy generates harvestable losses no matter how the market performs: when the market rises, short positions generate losses; when it falls, long positions do.

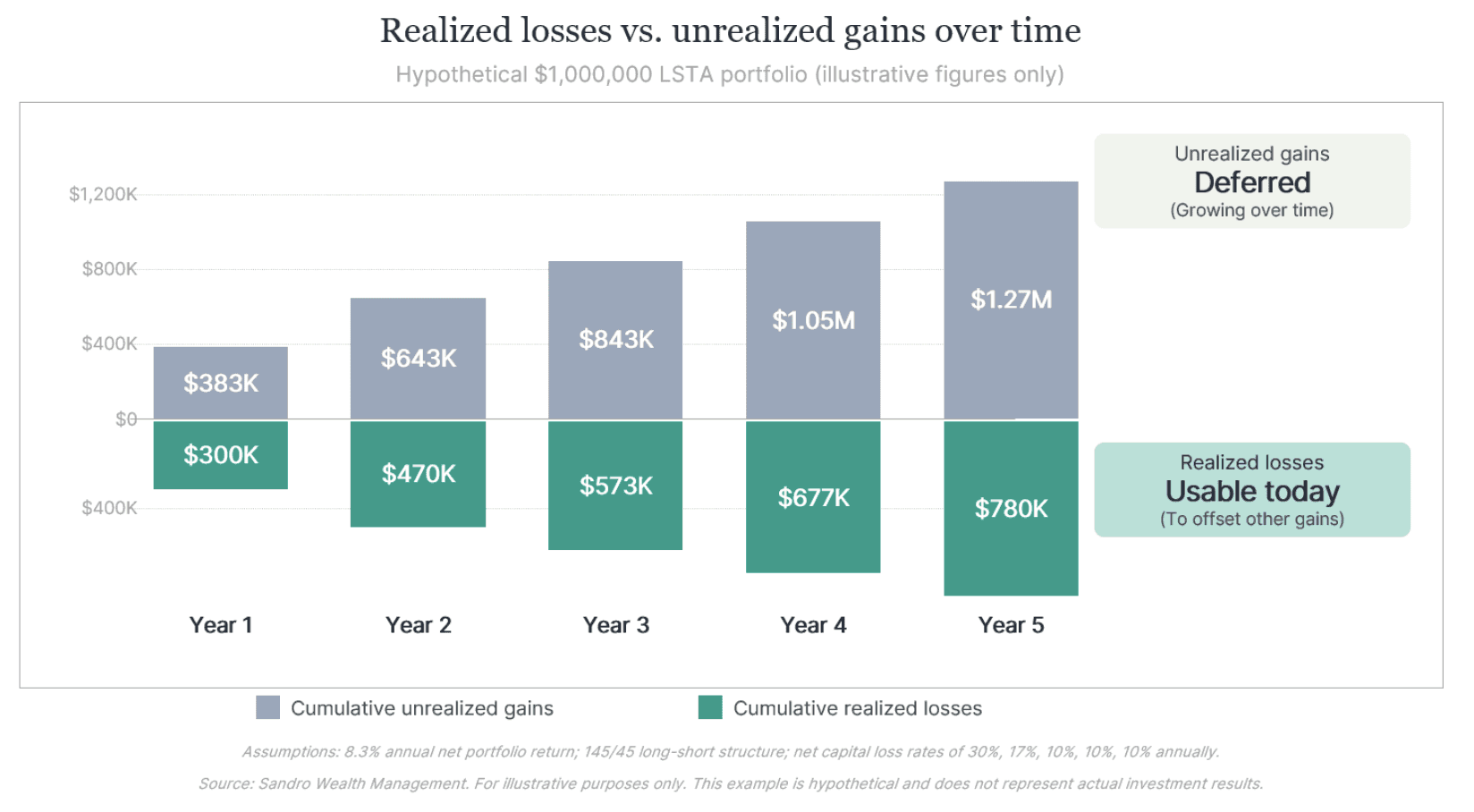

Over the years, the cumulative effect of the model’s choices can lead to substantial tax savings, all while the portfolio continues to deliver the potential for returns above the benchmark.

An Essential Distinction: Elimination vs. Deferral

At first glance, the strategy described above might appear to eliminate an investor’s tax burden entirely by accumulating capital losses. But that’s not the case.

The realized losses from selling losing positions are real and immediately usable. However, the gains on the portfolio’s winning positions remain. Capital gains on appreciated stocks in the portfolio will become taxable if and when those positions are sold.

Understanding this distinction is important. Under an LSTA strategy, taxes that are eliminated today (on realized losses) are offset by taxes that are due in the future (on unrealized gains). The investor receives an immediate tax benefit on one side while retaining a growing tax liability on the other. This is why LSTA strategies tend to be most suitable for long holding periods, where this deferred liability has the most opportunity to be reduced (or eliminated entirely).

As a result, LSTA only offers tax deferral, not tax elimination. However, deferral can still be a significantly powerful tax benefit – for three reasons:

1. Recognition Flexibility. Consider an investor who uses accumulated LSTA losses to offset gains from selling their business. In doing so, the investor has traded a tax obligation they can’t control – the business sale – for one they can. Gains from the LSTA portfolio can be recognized deliberately and on an investor’s own schedule.

2. Compounding Advantages. Deferring gains has a compounding benefit. Every dollar of tax not paid today remains invested in the portfolio, earning returns. Over a multi-year horizon, the cumulative value of compounding on deferred taxes can substantially increase final wealth.

3. Potential for Permanent Elimination. Perhaps most importantly, deferral can become permanent elimination under certain circumstances. If an investor’s portfolio becomes part of their estate, the cost basis of appreciated positions steps up to market value, and the deferred gains are never taxed. Alternatively, donating appreciated shares to a qualified charity allows the investor to claim a deduction at their market value.

While an LSTA strategy may not eliminate taxes entirely, it can meaningfully reshape when and how those taxes are paid. That creates the potential for planning decisions that align with an individual’s financial picture and enhance their after-tax wealth accumulation.

Conclusion: Final Considerations for LSTA Investors

LSTA strategies aren’t merely tax-loss harvesting engines; pre-tax alpha is also a necessary component of their success. The underlying structure involves financing costs and management fees. If the portfolio fails to generate returns sufficient to overcome these structural costs, the investor may be worse off than holding a passive index – regardless of tax benefits.

Furthermore, generating pre-tax alpha serves a legal function. In order to satisfy IRS rules, a tax-saving investment strategy must demonstrate a profit-seeking investment rationale. Without pre-tax alpha, an LSTA strategy risks being invalidated by the IRS.

Finally, it’s important to understand that the level of leverage within an LSTA structure can vary. Modest implementations target lower tracking errors and generate smaller annual losses. Aggressive use of leverage can generate significantly larger tax savings, but also lead to greater deviation from the underlying benchmark.

Ultimately, a long-short tax-aware strategy can make sense for investors navigating large tax liabilities, major liquidity events, or concentrated equity holdings. But given its complexities, LSTA investing is best evaluated as part of a comprehensive wealth plan. If you’re interested in exploring whether an LSTA strategy aligns with your specific portfolio objectives, please reach out to our team through the Sandro website.

Disclaimer

Sandro Wealth Management, LLC (“Sandro Wealth”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where Sandro Wealth and its representatives are properly licensed or exempt from licensure.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐ looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Targets are estimates based on certain assumptions and analysis made by the Advisor. There is no guarantee that the estimates will be achieved.

Although bonds generally present less short-term risk and volatility risk than stocks, bonds contain interest rate risks; the risk of issuer default; issuer credit risk; liquidity risk; and inflation risk.

Diversification does not ensure a profit or guarantee against loss. Past performance shown is not indicative of future results, which could differ substantially.

Investing in private funds involves a risk of loss that each existing and prospective investor should understand and be willing to bear. Existing and prospective investors are reminded to read fully and carefully understand these risks as outlined in Offering Documents and to discuss these risks with the Advisor.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor's particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. All investments include a risk of loss that clients should be prepared to bear. The principal risks of Sandro Wealth Management LLC strategies are disclosed in the publicly available Form ADV Part 2A.