At Sandro Wealth, we have long held the view that the United States economy holds sustainable structural advantages compared to the rest of the world. This view justifies significantly overweight portfolio allocations to US markets. As the chart below illustrates, a client invested in US public equities over the past five years would be significantly better off than a client invested in other regions of the world. While recent policy shifts have contributed to elevated market volatility and investment uncertainty, they have not undermined America’s enduring strengths.

Foundational to this view is empirical evidence showing the US as a leader in key categoriesresponsible for economic growth and financial stability. Under Sandro’s Global Investment Framework (GIF), five foundational forces drive a country’s long-term investment potential: Demographics, Institutional Policy, Innovation, Access to Capital, and Profitability. The results of our analysis, which reviews 18 countries that together account for 77% of world GDP, justify continued optimism in the United States as a preferred investment destination.

In the near term, tariff policy uncertainty will likely contribute to elevated volatility in US markets. The US also needs appropriate solutions for the country’s long-term challenges, including rising deficits and an evolving labor force. But despite these shifts, America’s structural advantages are too large to be eroded in such a short period. We believe this strong foundation will foster continued US exceptionalism in both public and private markets over our investment timeframe, a view that directly guides our asset allocation decisions in the Sandro Wealth Management Total Portfolio Approach.

Foundational Force #1: Demographics

Economic growth is most sustainable when driven by a young, productive, and growing population. This demographic makeup supports the steady expansion of a country’s labor force and consumer class. While the US faces similar demographic challenges to many advanced economies, several of America’s unique attributes can help the country navigate these challenges effectively.

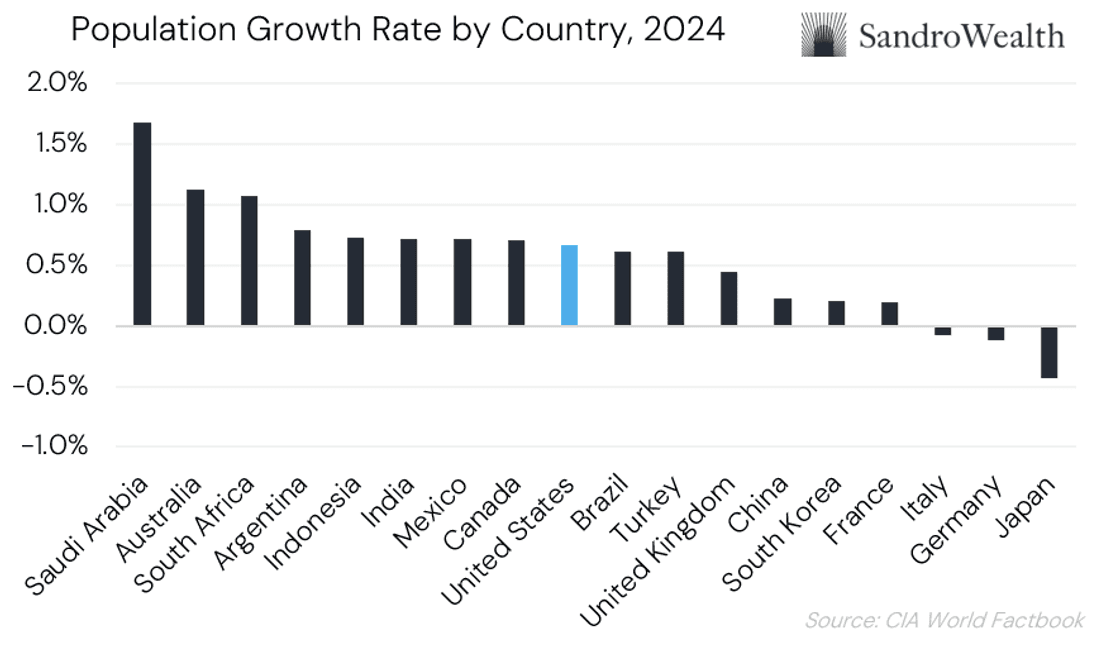

In terms of population growth, the US ranks ninth in our analysis. However, the US places well ahead of other developed countries, including Japan, France, and the United Kingdom. America also benefits from a highly productive population due to widespread technological diffusion.

When it comes to the total size of America’s working-age population, the country ranks only behind India and China. Notably, immigration has historically helped support the size ofAmerica’s labor force, meaning the current political environment could impose unique challenges. However, increased automation may be able to mitigate the economic impacts of reduced immigration.

America’s demographics are further enhanced by the high standard of living of US citizens. With the highest GDP per capita of any country in our study, America’s consumer class has ample disposable income to help support economic growth. While this support is slightly dampened by the country’s above-average income inequality, it still helps offset many of the demographic challenges facing advanced economies. Across all demographic factors combined, the US places second in our analysis.

Foundational Force #2: Institutional Policy

Transparent institutions and supportive policy measures are vitally important for an economy to prosper. Countries with politically controlled monetary policy often face elevated inflation risks. Meanwhile, extractive government institutions and high tax rates can disincentivize entrepreneurship and business expansion.

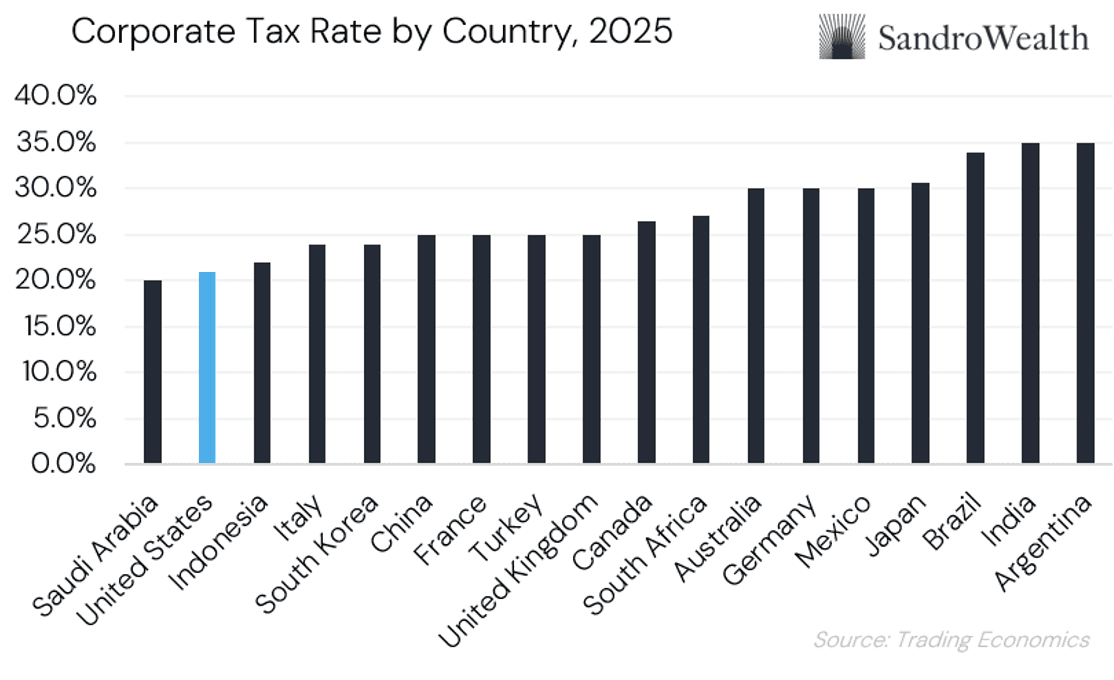

The US has historically provided above-average institutional support for economic growth and remains at the forefront of fiscal and monetary policy innovation. While the role of the Federal Reserve has been under debate recently, America’s central bank remains a highly independent institution. While inflation is currently elevated, this independence has helped keep long-term inflation expectations anchored in line with the Fed’s target. In addition, theUS has one of the lowest corporate tax rates of any major country.

Across all measures of institutional quality, the US ranks fifth in our analysis, closely trailing Japan and Germany. For the US to remain a preferred investment destination, the country must remain open, transparent, and aligned with international law. However, the type of government wealth extraction that occurs via excessive taxes or outright nationalization appears unlikely to take place in the US.

Another notable area of policy risk for the US is the federal deficit. In the recent past, the US deficit has averaged about 5% of GDP annually, an unsustainably high level. While we areconcerned about rising public spending projections for the US, we also see a pathway for higher GDP growth to shrink this deficit over time. A US debt crisis does not appear likely within our investment timeframe.

Foundational Force #3: Innovation

Innovation drives productivity gains, creates new jobs, and ultimately leads to higher standards of living. A country’s capacity for innovation spans both cultural and institutional factors. Not only must individuals be willing to take the risk of developing new technologies,but they must also be confident that they will be able to profit from such innovations.

The US has been the global leader in innovation for decades, supported by both of these elements. Across patent, trademark, and industrial design filings, the US places second to China. However, more qualitative measures indicate that the US far surpasses China in terms of entrepreneurial culture. Overall, the US ranks first in our innovation analysis.

This capacity for innovation is perhaps best exemplified by America’s astounding 656 private startups with over a $1 billion valuation. In comparison, China has just 168. Further evidence can be found in America’s profit share within the technology sector. Of the top 50 tech companies in the world, US-based firms account for 49% of total revenue and 65%

of total income.

In recent years, China has significantly narrowed the gap with the US in the development of many advanced technologies. However, recent innovation in AI could create a significant discontinuity that places the US firmly in the driver’s seat. The high profits of US tech firms create more capacity to reinvest money into capital-intensive AI development, and many

of the leading AI companies continue to be drawn to the network effects of Silicon Valley.

Foundational Force #4: Access to Capital

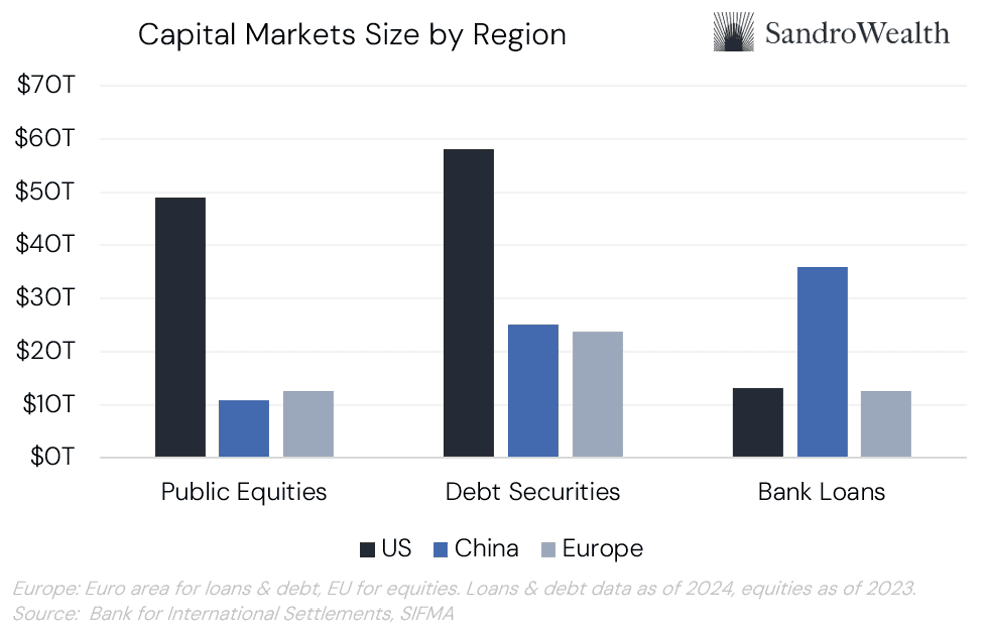

For businesses and entrepreneurs to undertake new initiatives, they need capital to fund their projects. Therefore, access to capital is an essential driver for economic growth. As home to the world’s deepest and most liquid capital markets, the US ranks first in this category.

America’s public equity markets are the largest in the world, eclipsing the value of Chinese markets by over 4 times and European markets by over 3 times. Moreover, America’s debt securities market is more than double the size of either China or Europe. While much of the US bond market is dominated by government securities, US corporations issue approximately $1.5 trillion in debt each year, indicating robust access to capital.

And this access goes beyond just public markets – America’s private markets are the largest and most sophisticated in the world. In 2024, outstanding private credit loans in theUS amounted to over $1 trillion, more than six times the rest of the world combined. Moreover, the US offers robust access to traditional bank credit, both for consumers and smaller firms. As of 2024, the US banking system had over $13 trillion in credit outstanding to non-financial firms, on par with Europe and second only to China.

Recent tariff and trade tensions raise a valid concern about the impact these policies may have on demand for dollar assets. Due to the dollar’s entrenched status as the dominant currency for global trade and finance and global reserve currency, however, international entities often have a structural need to invest in US markets. While the dollar’s dominance will likely see some erosion in the coming years, we do not see demand for dollar assets waning significantly, as there is currently no viable alternative reserve currency.

Foundational Force #5: Profitability

Profitability is a key driver of investor returns. High-margin business activities are able to support higher dividend and interest payments to investors. Moreover, these profits can bereinvested into business expansion to drive further growth and capital appreciation.

Under standard economic models, mature economies like the US tend to grow more slowly than their developing peers. However, the US benefits from exposure to high-profit industries like technology and a broad range of services. Many of these sectors can be less sensitive to economic cycles than commodity or manufacturing-based industries, leading to steadier growth.

In part due to this sectoral composition, the US is highly competitive in terms of business profitability. Net margins in the US are far greater than many other developed markets and often exceed developing markets too. As a result, America is among the global leaders in terms of five-year historical and forecasted earnings per share growth.

This earnings growth will likely be supported by the robust expansion of the US economy. According to the International Monetary Fund’s World Economic Outlook, the US is expected to see GDP growth averaging 2.0% annually through 2030. That is the second-highest figure among all developed countries in our sample.

Looking forward, US firms have the potential to expand their profitability with the increaseddeployment of AI tools. With many of the leading AI firms located in the country, America may have a first-mover advantage when it comes to integrating AI with business processes. This advantage is one factor supporting strong US earnings forecasts over the next several years, a key element in our GIF profitability analysis.

Conclusion: American Exceptionalism

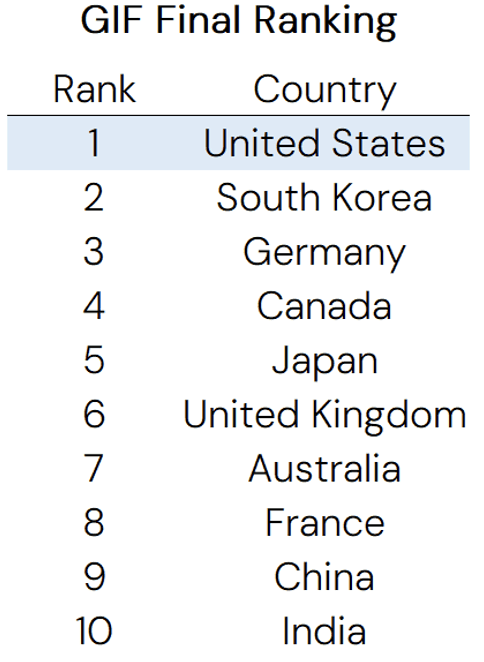

Based on these five forces, the US ranks first in Sandro’s Global Investment Framework, eclipsing the 17 other countries analyzed. This lead is robust, ranking 26% ahead of runner-up South Korea and 42% ahead of the median score. As a result of this analysis, Sandro currently has zero weight to non-US equities within client portfolios.

While many have pointed to high valuations as a reason to move away from US investments, we believe this perspective is short-sighted. We agree that valuations in the US are high on both an absolute and relative basis, but we also believe that these valuationsare justified. As we have demonstrated in our GIF analysis, America’s structural advantages create the potential for faster expansion than other markets. Perhaps most importantly, America’s historical return on equity is 40% higher than the average of all countries in our sample, offering substantial opportunity for US firms to reinvest capital to accelerate growth.

While recent headwinds have not changed our perspective on the US, future challenges could. If the global economy grows faster than anticipated, investors may be able to benefitfrom international markets, which typically have greater exposure to cyclical industries. In addition, escalating conflicts between America and China could disrupt US tech supply chains and lead to weaker forecasted earnings growth. But for the time being, we do not see compelling reasons to shift our exposure internationally.

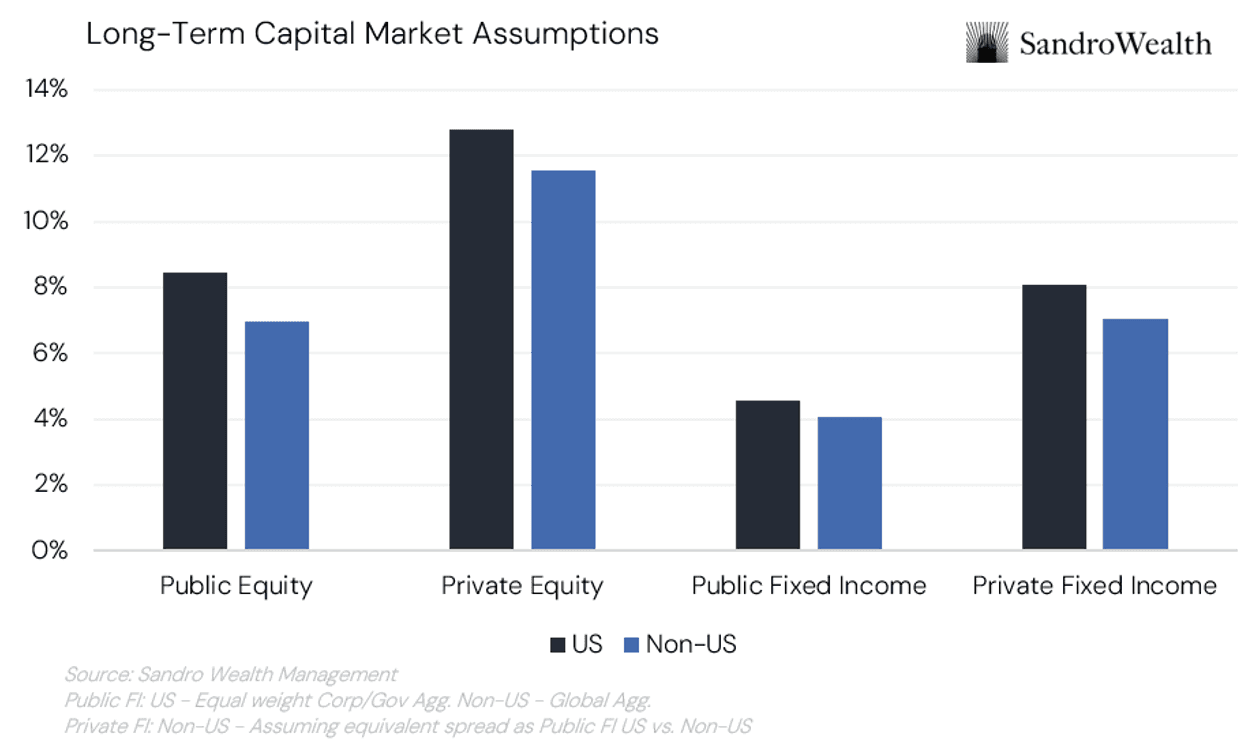

Importantly, America’s investment advantages are not limited to public markets. The forceswe listed today are just as relevant to asset classes like private credit and private equity. Inline with Sandro’s Total Portfolio Approach, we believe that private market allocations can potentially help investors more effectively achieve goals like wealth creation, higher income, and lower volatility. As in public markets, our GIF analysis demonstrates that investors will likely benefit from keeping their private market allocation heavily weighted to the US.

Methodology

Sandro’s Global Investment Framework (GIF) is a proprietary quantitative analysis of comparative investability covering the G20 members, excluding Russia, the European Union, and the African Union. This analysis was conducted by scoring each country along five categories: Demographics, Institutional Policy, Innovation, Access to Capital, and Profitability. These scores were calculated by ranking each country along six to ten subcategories within each category, and then summing those scores to create a total ranking.

For example, Demographics contains eight subcategories, including Working Age Cohort Growth and Real GDP per Capita. A country that placed first in each subcategory would earn a Demographic score of 8, while a country that placed last in each subcategory wouldearn a Demographic score of 144. Thus, lower scores translate into higher investment potential under GIF.

Data was aggregated from sources deemed authoritative, including the World Bank and the Bank for International Settlements. Where data was not available for a particular country, the country was ranked last or had prior year data pulled forward. All category scores were calculated using simple summation, except for profitability, where a weighted average was used to prioritize earnings estimates and a scaling factor was used to normalize the score’s magnitude.

Related INSIGHTS